Just before you picked up this issue of Growing for Market, you likely were at your desk or computer planning out the growing season: What you will plant and where, and what supplies you’ll need to prepare for the growing season. Maybe you just charged a bunch of purchases to your credit card or scheduled payments from your bank.

You may have a big picture plan that works: Your projected revenue for the year will exceed expected expenses, as well as loan repayments and capital improvements. You’ll show a profit for the year. Great! But the challenge for many market gardeners is that the expenses (and cash payments) are front-loaded in the first half of the year, and the revenues (and cash inflows) don’t start to peak until the second half of the year.

In April, your bank balance may dwindle down to a precarious level while your credit card balances ramp up. Sure, it will all work out by the end of the year — if you can get there. You need to be able to sustain operations by paying your employees and vendors on time. It can be overwhelming.

Certainly, there are ways to mitigate the cash flow stress (from season extension to selling CSA shares). That said, the best way to ease the stress is to create a cash flow budget that lays out a clear plan to stay “cash positive” throughout the year — that is, to always have a positive balance in your bank account.

A cash flow budget maps when you expect the cash to come into your business and when you expect it to leave. It helps you predict when cash will be tight so you can create a plan to manage it. If you’re planning a big purchase (maybe you want to build another greenhouse) a cash flow budget can help you time purchases, loans, and loan repayments so that you don’t jeopardize your financial position.

A well-thought-out budget clarifies that you can make it through the year without getting into trouble.

The cash flow budget also gives you a benchmark to help you stay on track. Let’s say you build into your plan a target of $1,500 in sales at each farmers market. At the end of each market, you can look at your sales to see if you achieved that goal. If not, you can strategically adjust on the spot — whether its hustling sales to make up the difference, cutting back on expenses because your sales fell short, or focusing on your production because you didn’t harvest as much as you needed.

In other words, a cash flow budget gives you the tools to stay on track, avoid a cash crisis, farm with intention, and alleviate stress. And, you can create a plan in a few hours.

Before you get started, consider your goals. Do you have a profit goal (say, $50,000)? Do you have a production goal (for example, expand to grow on another acre)? Knowing where you want to be at the end of the year is the best way to create a plan to get there.

As you think about the coming year and your goals, it can help to review last year’s sales and expenses. How much did you sell of what products and to which customers? How much did it cost to produce all those flowers and vegetables? How much labor did you have? What would you do differently, and what would you keep the same?

Also think about how much of a cash buffer you want to have at any given time? Is $1,000 in the bank enough of a cushion? Maybe you need $10,000. You don’t want your bank balances to get too close to zero. Your actual cash flows will be off one way or another: A payment from a customer may be a few days late. You may need to make a purchase a few weeks earlier than planned. You want a buffer to absorb the unexpected shifts.

Steps to create a cash flow budget

I usually recommend creating a cash flow budget in two phases. In the first phase, plan out the year, big picture. That is, what’s your plan for revenue for the year? How much do you want to budget for production expenses, selling costs, labor, and overhead? You want to make sure that your annual plan gets you to your desired goal.

Once you have an annual budget, you can move onto the second phase and break it down into a monthly cash flow budget. As you know, the cash doesn’t flow evenly into and out of your business; it happens in waves. You’ll want to make sure you can get through the traditionally lean times (April – June).

PHASE ONE: PLAN THE YEAR

1) Forecast sales

There are two ways to create a sales forecast: start with your revenue goals (top-down) or start with specific production goals (bottom-up).

Top-down sales projections

For a farm that has been in business for a while, it can be more efficient to start with a revenue goal. One way to set a revenue goal is to calculate your breakeven sales. I detail that process in “The magic of breakeven and how it can help set sales goals” in the February 2020 GFM. The other option is to set a target growth rate, for example, you want to grow 11 percent from $90,000 to $100,000.

From the big picture number, you can break it down further — how much sales do you anticipate earning from the different revenue streams, for instance, attending farmers markets or selling wholesale? If you decide, for example, that 75 percent of your revenue will come from farmers markets and 25 percent from wholesale, then you need to earn $75,000 from the farmers markets and $25,000 from wholesale.

Knowing how much you’ll sell in each sales channel (or customer group) can help you think through monthly cash flow as well as production plans. CSA prepayments usually come in the first half of the year before you have any crops. Farmers market sales happen later in the year, and you usually get the payments right away (either cash or credit card direct deposits). Wholesale customers often pay several weeks after delivery.

Bottom-up sales projections

If you don’t have a lot of experience setting sales goals, especially in the first few years of a farm business, it can be easier to start from the bottom up.

- How many wholesale customers do you want? How much do you expect them to order each week? How long is your season?

- How many CSA subscribers do you think you can grow produce for?

- How many acres do you want to plant? How much can you produce in each bed or row? And how much revenue can you earn from each crop.

For example, if you think you can grow enough produce for 40 CSA members and your price will be $700 per share, then your estimated revenue from the CSA would be $28,000.

2) Estimate expenses

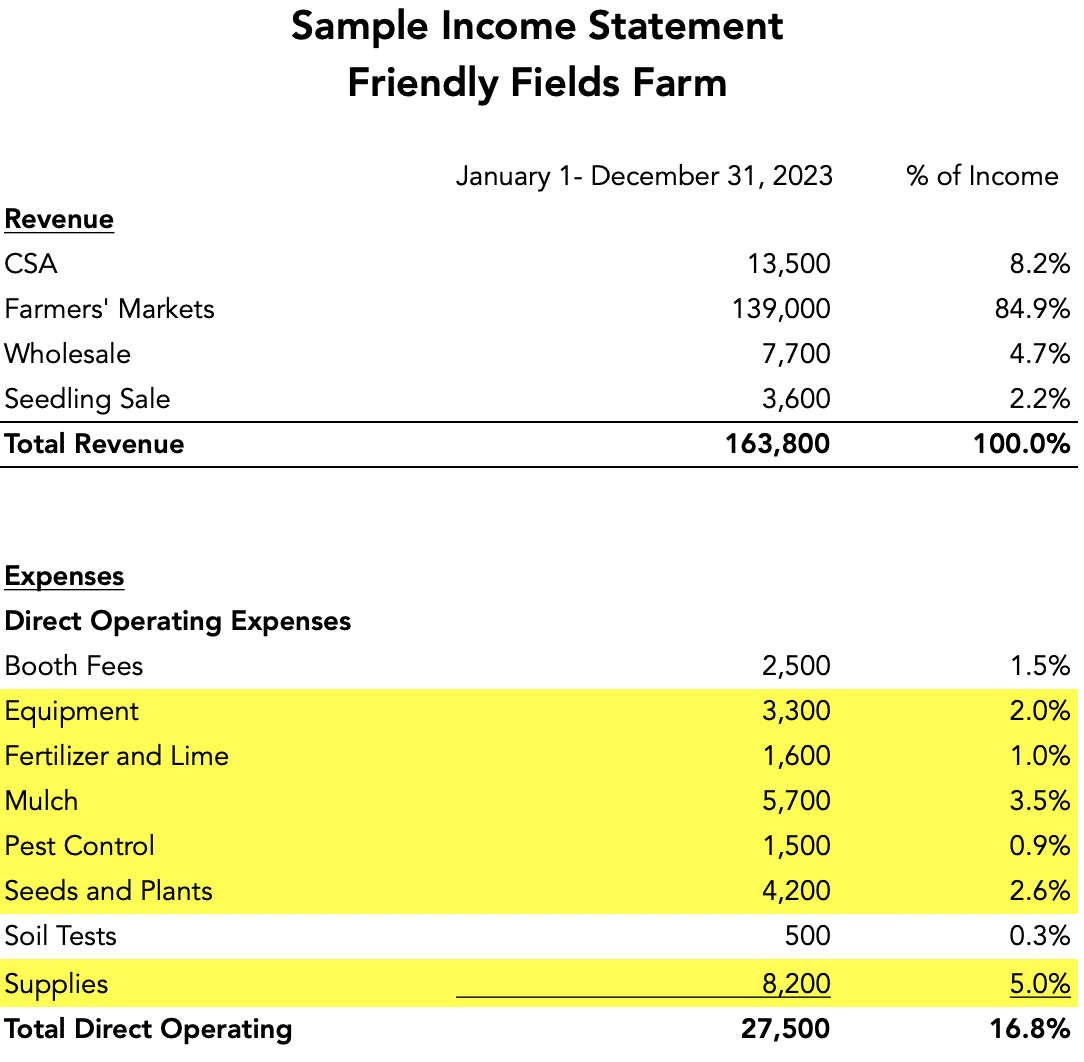

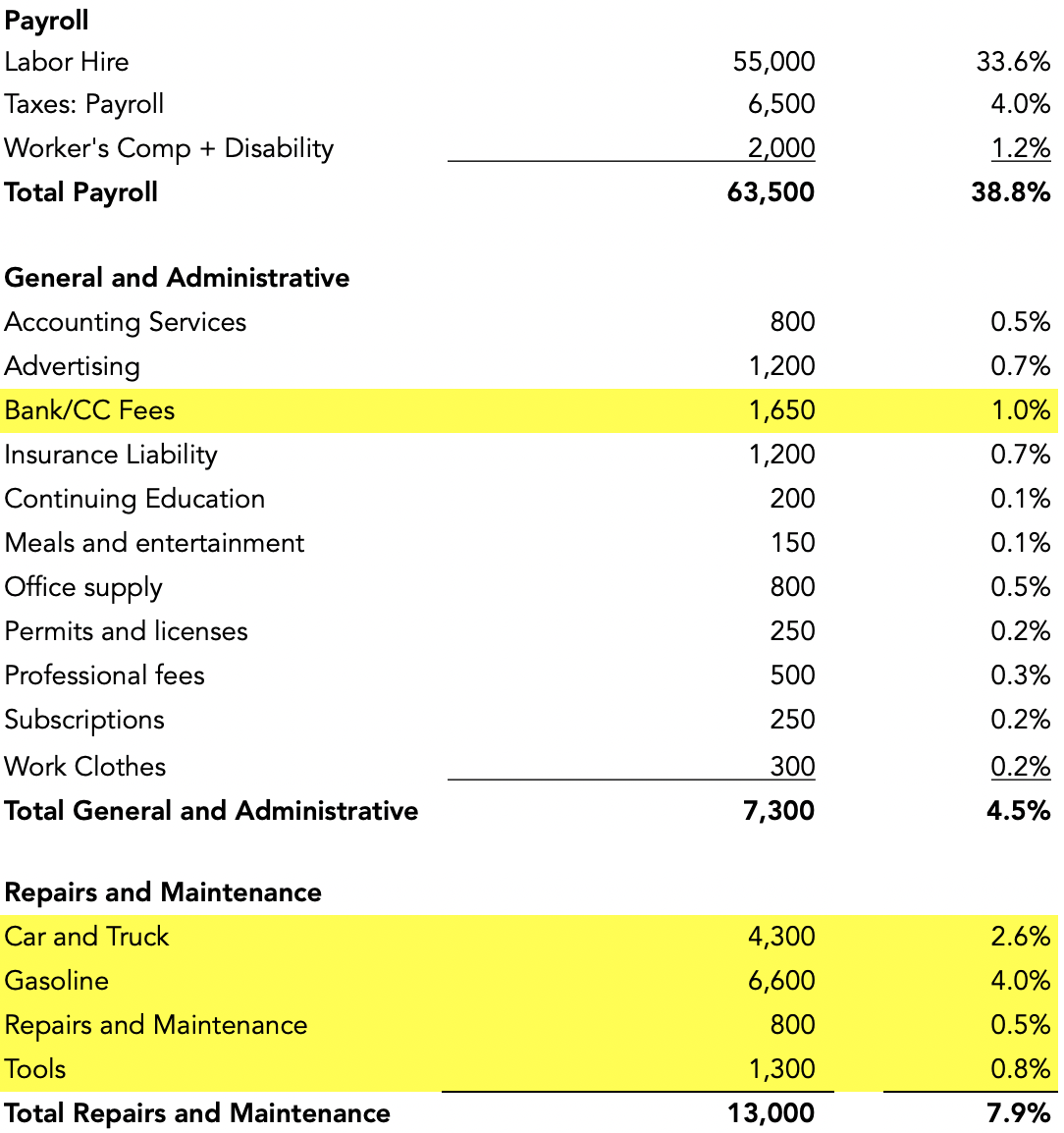

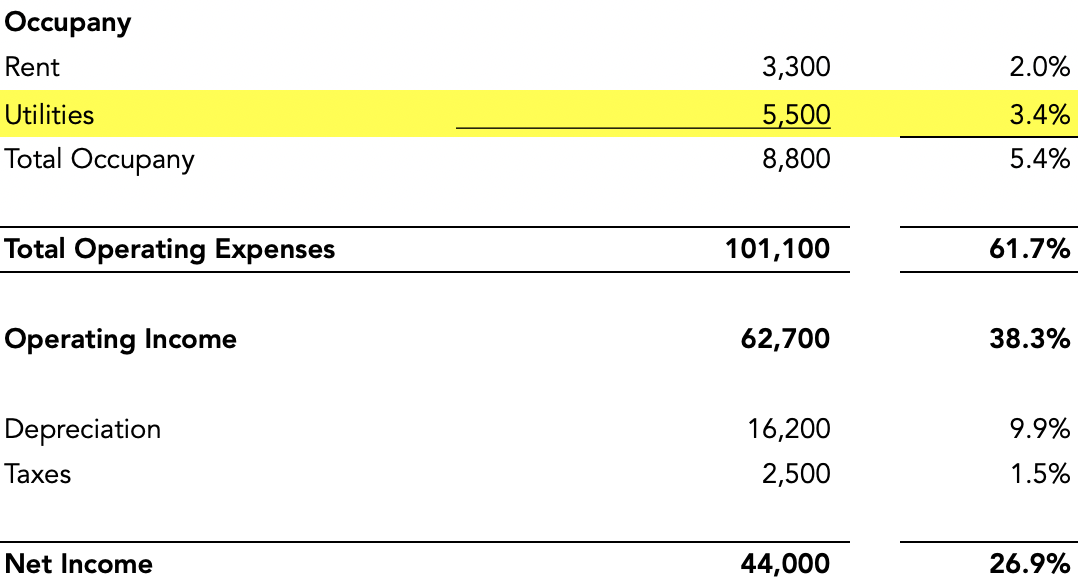

Take a look at 2023’s profit and loss statement, and specifically at your expenses. Consider which expenses are associated with production and sales and which are general overhead (we’ll talk about labor expenses in a minute). Specifically, if you increase sales, which expenses will also increase? In academic terms, these are your variable expenses- see figure 1 for an example of how this might look.

Your production costs can be seeds, greenhouse supplies, field supplies, and labor. For the purposes of cash flow planning, you can expect that as revenue and production increases, you will spend more on these line items. You will also have more credit card processing fees and packaging. If you’re using QuickBooks, you can run a profit and loss statement for last year, and add a column to look at expenses as a percentage of revenue.

For each line item, take the percentage from last year and multiply it by this year’s sales projection. For example, if your seed/seedling expenses were 3 percent of revenue last year; then it’s reasonable to expect they will also be 3 percent of revenue for the coming year. If you project sales of $100,000 for this year, then you can budget for $3,000 in seed/seedling expense for the year.

I know it might feel tedious, but I encourage you to go through each line item in your profit and loss statement. This ensures that you don’t forget anything.

One of your biggest expenses will be payroll, so you want to make sure you think this through. If you set a budget for $30,000, how many workers can you have? Is that enough to support your sales goals? Will you pay payroll taxes and workers’ comp insurance?

A sample schedule provides a framework for estimating labor expenses.

List out the different positions you need filled: harvesters, CSA managers, farmers market crew, drivers, etc. You don’t need to know who’s going to be working when, just that someone will be working.

- Set the hourly wage for each position.

- How many people do you need working each shift, each day?

- How many hours will they work in a day? How many days per week? And for what weeks throughout the year.

Once you determine the number of shifts worked per week, the duration of each shift and the hourly pay, you can then calculate an estimated weekly payroll expense. You may need to adjust the schedule for different phases of the growing and selling season.

In addition to the wages paid to your employees, you will also pay federal and state taxes, social security, and workers’ comp insurance on behalf of your employees. This can vary from 9 percent to 12 percent in additional expenses. For simplicity’s sake when creating a budget, add 11 percent to the salaries for payroll withholdings and insurance. For actual day-to-day operations, I encourage you to seek a payroll service provider to ensure that you are properly withholding payroll taxes and submitting them to the appropriate agencies.

Finally, outline your non-production expenses (like liability insurance, vehicle registration, etc); you can budget more generally. You know how much your liability insurance will be. You can project these expenses based on what you spent last year. If you know an expense will go up, then you can factor that in, too.

3) Detail other cash flows

So far, we’ve been focused on the core of your business. But you’ll likely have other cash flows. If you have a loan, then you’ll have regular payments. If you’re trying to pay down your credit cards, you’ll want to set a goal for that, too. If you plan to purchase equipment or make significant improvements to infrastructure, then list those out, too. If you expect to get a grant, write that down.

One more thing — and this is really important — write down what you want to pay yourself. If you haven’t already included a salary for yourself above, then note it here. What do you need to support yourself? You need to cover your basic living expenses as well as pay your personal debt. Ideally, you’ll also include a savings goal (retirement) and factor in that you’ll want to do things besides work (hello, vacation!), and you’ll need some funds for that.

4) Look at the year as a whole

At this point, you should have an annual total for sales, expenses, and other cash flows. Take your total sales number (and grants), and then subtract your expenses and other cash outflows. Do you have a positive number? In other words, is your projected revenue and cash inflows enough to cover your expenses, loan repayments, and personal expenses?

If revenue isn’t enough at this point, then you’ll need to refine your numbers to make it work. You have a few options:

- Consider if you need to increase your revenue goals. Can you practically get there production-wise?

- Can you reduce your operating expenses? Look at each line item and consider where you can reasonably make it work with a tighter budget.

- Do you need to take a loan to cover your desired investments/purchases for growing the business?

For deeper analysis, you may want to look at your pricing strategies and cost of production. Are you pricing your products high enough so that you can cover your costs? If you don’t know your cost of production, then this will be difficult to answer. Josh Volk wrote a great article on “Know your cost to grow” in the November 2023 GFM.

You’ll need to find a scenario where you have enough revenue and cash inflows to cover your expenses and other cash outflows. If you can’t make it work on paper here and now, then the chances of you making it work in real time is slim to none.

PHASE TWO: CREATE A MONTHLY BUDGET

Now that you have an annual budget, we can break it down into a monthly cash flow plan. In what months do you expect the cash flow?

5) Assuming that you created your annual budget in Excel or Google Sheets, add 12 columns to the right of your annual budget, one for each month. Then map out, by month, when you expect to the cash to flow.

For example, if you projected that you’d earn $75,000 from farmers market sales, when do you think that will happen? If the markets don’t start until June, then start laying out the farmers market revenue for June on. If you expect that all your production purchases will happen in February and March, then put all of those budget expenses in those months. See figure 2 for an example of how this might work.

6) At the bottom of each month, you can total the expected income and other cash inflows and the expected expenses and cash outflows. Your net cash flow will be inflows minus outflows. It’s okay if you have some months with a negative cash flow (for example, expenses exceed revenue). It’s expected in a seasonal business. The trick is to make sure you have enough cash in the bank to float those months.

7) Note how much cash you have at the beginning of the year. This is your beginning cash balance. At the bottom of the January column, take your beginning cash balance and add (or subtract) the net cash flow for the month. This is your ending cash balance for the month. Does it remain positive with a cash balance greater than what you want your buffer to be? Great! If not, then you’ll need to consider if you need to borrow cash or adjust the timing of your purchases.

8) For February, your beginning cash balance is the ending cash balance for January. Add (or subtract) the net cash flow for February. This is your projected ending cash balance for February. Does it remain positive? Great! If not, then you’ll need to consider if you need to borrow cash or adjust the timing of your purchases.

9) Continue on in this way through the rest of the year; confirm each month that your plan keeps you cash positive with enough of a buffer. Make adjustments as necessary.

Now what?

You’ve created a plan that you know can work, and you have a road map to help you stay on track. Each month, you’ll want to compare this budget to what actually happens.

Did you achieve your CSA sales goals in March? Did you sell what you expected at the seedling sale in May or the farmers market in July? If not, do you know why? How can you make up the difference? If you miss the mark on your sales goals, then what other adjustments do you need to make? Do you need to cut back on expenses, or increase production? Do you need to find additional customers and markets?

Also, look at your expenses on a monthly basis to make sure you stick to the budget. Did you overspend in certain areas? What adjustments do you need to make to get back on track? If your costs increased and you hadn’t planned for it, then maybe you need to raise prices. If you overspent, then maybe you need to rein it in in other areas.

In summary

This focused approach helps anticipate cash fluctuations, allowing you to strategize for lean periods and always maintain a positive cash balance. Regular monitoring of actual performance against the budget enables you to adjust and adapt quickly, whether by tweaking sales approaches, managing expenses, or revising production plans. Ultimately, this proactive budgeting approach empowers you to navigate cash flow challenges, farm intentionally, and mitigate financial stress while working towards your goals.

If you need more support, I invite you to visit my website thefarmersoffice.com. I have a video tutorial that walks through this process step-by-step.

Julia Shanks is the author of The Farmer’s Office, Second Edition and The Farmers Market Cookbook, available from growingformarket.com/. She works with farming and food entrepreneurs to help them achieve financial sustainability through business planning, cash flow planning and financial feasibility studies. She is a Certified QuickBooks Pro Advisor. You can learn more about her work and watch videos on how to create a cash flow budget at thefarmersoffice.com.

Copyright Growing For Market Magazine.

All rights reserved. No portion of this article may be copied

in any manner for use other than by the subscriber without

permission from the publisher.