With the end of the year in sight, it’s time to start thinking about evaluating your farm’s business performance for the year – and that means it’s time to think about the creation of the three key financial documents that provide a picture of the financial state of your business: the balance sheet to show your overall financial position; the income statement to show your financial performance for the previous year; and the statement of cash flows to describe the way money – including loan proceeds, debt service, and family living expenses – moves through your business.

When assembled on the first day of the fiscal year (January 1 for most of us) year after year, these three documents tell the financial story of your farm and farm business. The process isn’t just for experienced farmers – anybody with a farm business can benefit from creating annual financial statements, and I recommend that beginning farmers do it from day one. Even if you aren’t farming yet, you can use these financial statements to evaluate your personal financial situation so that you can measure the changes that result when you do start.

Too many people avoid financial statements. For some, the statements seem too complicated – we’re going to try to help with that here. Others don’t see how the financial statements add value to the farm. And while I know a few farmers who have been successful over the long haul who have never drawn up financial statements, the annual, objective evaluation of your farm finances is a straightforward system that can improve your overall odds of financial success and sustainability.

While money is not the only metric for success, it is a key metric. Making money lets you do other cool things, like grow great vegetables for people to eat, so the money on your farm matters. When you put the time into creating and understanding your financial statements as something more than a way to get a loan or fulfill your obligation to the IRS, you treat your business like a business. And treating your business like a business not only helps you stay in business; it also helps bankers, investors, and other financially interested parties understand your business, and shows them that you take using their money seriously.

But more importantly, meaningful financial statements can help you anticipate and evaluate problems and barriers to success. For example, from your balance sheet, you can use the current ratio, which compares what you have on hand to what you owe in the next year, to anticipate the potential for cash flow problems. Comparing adjusted income statements from one year to the next helps you understand your farm’s actual performance, even if your checkbook makes it look like you didn’t do very well because you bought your boxes for next year in December. And the statement of cash flows can help you understand why, even though you brought in more in revenues than you spent on expenses, you never seem to have enough money in the checking account.

This month, I’ll provide background information on the different financial statements and how they’re constructed; in November, I’ll help you gather, manipulate, and use the data to create and interpret them.

Please note that you may be asked to provide financial statements in different forms to different people. A banker may want your financial statements in a different format than an investor, and the IRS will want an income statement – in the form of a Schedule F – that differs significantly from the format presented here. But if you’ve done the work to create the statements as they’re described here, you’ll have the raw numbers that you need to quickly create statements in different formats for different audiences.

Also, please don’t just hit “print” on the corollary reports in QuickBooks and call this job done. For the reports in QuickBooks to be meaningful and accurate, you have to do a lot more accounting work than most small farmers do – I recommend using QuickBooks as a bookkeeping program throughout the year, then extracting numbers from it to create these reports in a spreadsheet program such as Excel, Numbers, or Sheets.

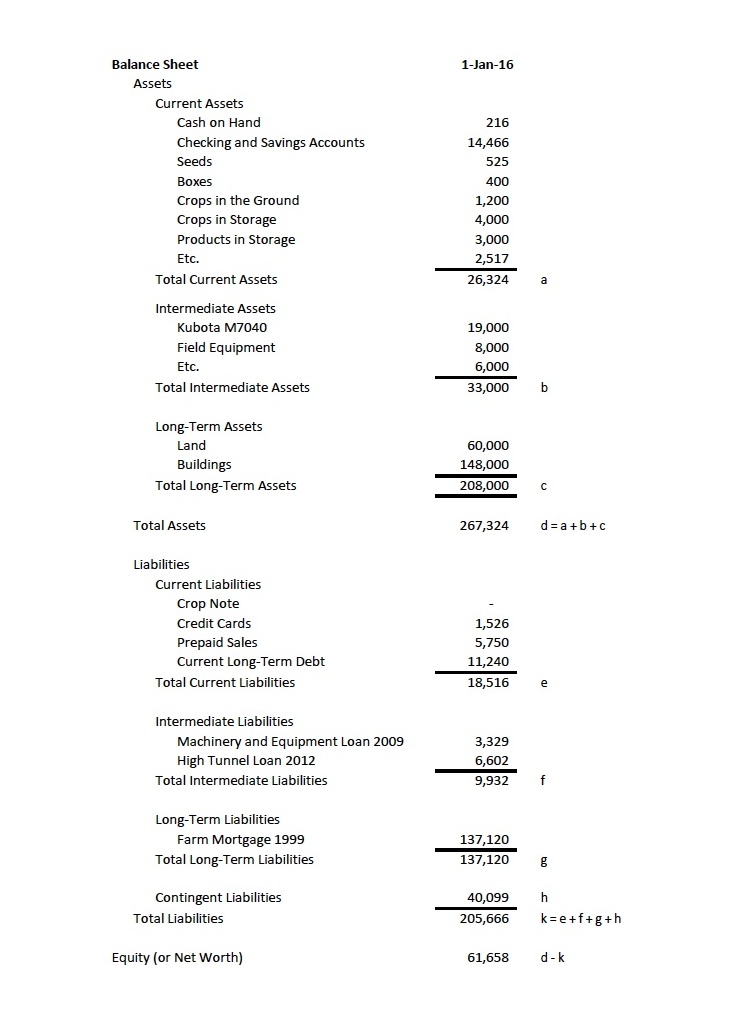

The Balance Sheet The balance sheet provides a snapshot at one particular point in time of all of the things you have (your assets), the obligations you have to fulfill (your liabilities), and the difference between the two (your equity).

The balance sheet provides a snapshot at one particular point in time of all of the things you have (your assets), the obligations you have to fulfill (your liabilities), and the difference between the two (your equity).

All business balance sheets divide what you own and what you owe into different categories according to their expected lifespan. Conventional balance sheets use current (also known as short-term) and long-term categories; farm balance sheets add an additional intermediate category.

Farm balance sheets use some other conventions that differ from those of non-agricultural enterprises. Farm balance sheets use market value rather than a cost basis to value assets; in other words, farm balance sheets determine how much your assets are worth according to what you can sell them for, rather than using a calculation for depreciation. And farm balance sheets do not usually include entries for “goodwill” or “blue sky” – the amount that a business may be worth to a buyer over and above its hard assets because of its customers or market reputation.

Also, farm balance sheets do not usually include entries for “goodwill,” or the amount that a business is worth over and above its hard assets. Goodwill refers to the value of things like customers, market reputation, and business systems; farm balance sheets just reflect what the farm can be sold for as its individual parts.

Current assets are things that you use up to create cash in the coming year. In addition to the cash that you have on hand and the money in your bank account, current assets include consumable production supplies such as seeds, fertilizer, fuel, and boxes; annual or overwintered crops that you have in the ground, such as spinach for overwintering or garlic for harvest next summer; annual and perennial stock that you have in the greenhouse or cooler that will go in the field next year; and crops and products that you have in storage. They also include supplies that you’ve paid for but don’t have, such as prepaid fertilizer or potting soil that has not been delivered yet.

In a livestock enterprise, we would also include market livestock, such as lambs and steers, as current assets, because we plan to use them up this year, rather than using them to create more lambs and steers. Feed and medicine on hand would also be considered current assets.

Current assets also include accounts receivable. Also known by its abbreviation, AR, accounts receivable are payments you expect to receive, but which have not been paid yet, for the delivery of product of products or services that you have already made. For most market farmers, AR is simply the sum of invoices that have been issued but not yet paid.

Current liabilities are the obligations you have to fulfill in the coming year. These obligations include any annual operating expenses that are due in the coming year, as well as credit card balances – even if you owe more on your credit cards than you plan to pay off in the coming year, the balance is still considered to be a current liability unless you have a long-term payment plan.

Current liabilities include the principal due during the coming year on intermediate- and long-term liabilities. We only include the principal, without the interest, because the balance sheet is a snapshot in time, you don’t owe the interest on those loans until you haven’t paid back the principal.

If you have any accounts payable – money you owe for bills that you’ve received but haven’t paid yet, also called AP – that goes on your current liabilities as well.

Current liabilities also include any prepaid sales to be delivered in the coming year. If you’ve taken money for CSA shares in October that you plan to deliver in May, you’ve created a financial obligation to your customers: you have to provide them with something valuable next summer. On the balance sheet, it’s no different than taking out a loan; you just get to pay this one off with vegetables instead of cash.

Intermediate assets are things that are expected to last for between one and ten years – assets like perennial plants, breeding livestock, tractors, and vehicles. I like to think of intermediate assets as things that are expected to create an ongoing stream of future value – tractors to grow the crops, ewes to crank out lambs, barrel washers to create clean carrots – that can be sold separately from the farm itself.

Ten years is a somewhat arbitrary upper limit – tractors that have lasted for forty years and still show no signs of giving up the ghost are still considered to be intermediate assets.

Long-term assets, also known as “fixed” assets, are those that have a life longer than ten years – usually limited to land and buildings. Long-term liabilities are the outstanding debt against these long-term assets. As with intermediate liabilities, only the amount of debt remaining after the current year’s principal payment is deducted is included in long-term liabilities.

A balance sheet should also include contingent liabilities to cover the financial liabilities that would result from liquidating assets, such as capital gains taxes and real estate commissions.

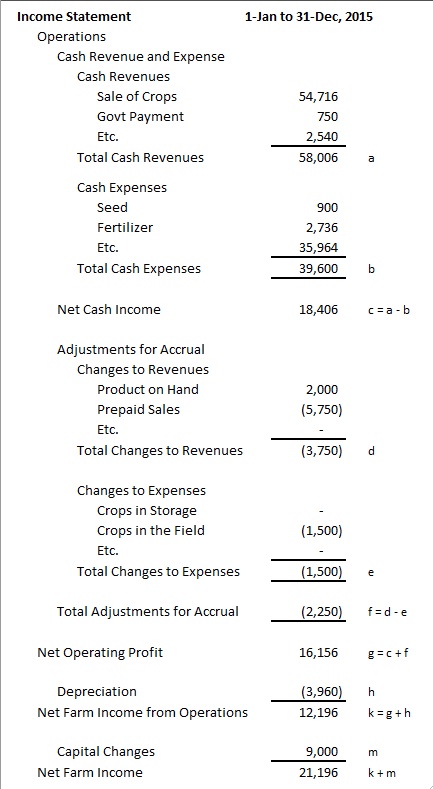

The Income Statement The income statement answers the question, “How did my farm perform this year?” How much did your farm give you in exchange for your labor, expertise, and capital risk?

The income statement answers the question, “How did my farm perform this year?” How much did your farm give you in exchange for your labor, expertise, and capital risk?

An income statement evaluates change over a period of time – usually from January 1 to December 31. Cash changes by how much you took in as revenues, and how much you sent out as expenses; but the farm income statement also includes adjustments for other changes, as well, in order to remove the variability that results from the timing of purchases and sales.

Because of these adjustments, you’ll need a balance sheet from the beginning of the year, a balance sheet for the end of the year, and your accounting program’s profit and loss statement or the Schedule F.

I like to start an income statement with the cash revenue and expenses: the payments you took in for the farm products you sold and the services you performed, and the cash you paid out for the normal operating expenses of the farm business.

Cash revenue includes the money you made from actually selling stuff, as well as government payments, grant income, sales of livestock, and crop insurance. Don’t include the sale of capital assets here.

Cash expenses include the normal operating expenses of a farm business – seeds, fertilizer, fuel, payroll, land rent or property taxes, and so forth. Include interest on loans or credit cards (which is basically rent on the bank’s money), but not principal payments. Do not include income tax or the farmer’s social security payments – those are the farm owner’s financial responsibilities, not the farm’s.

The difference between cash revenues and cash expenses is the farm’s net cash income.

Once the cash portion of the statement is established, it’s time to move on to the adjustments. The adjustments are made on the basis of the changes in current assets that have happened over the course of the year – these are the same current assets that were listed on the balance sheet.

For example, if you had $1,000 worth of cleaned and packaged vegetables on January 1, and now, on December 31, you’ve got $3,000 worth of cleaned and packaged vegetables, you’ve increased your saleable inventory by $2,000. But even though you’ve spent a bunch of money to produce those vegetables, you haven’t received any cash for them; if you don’t make an adjustment on your income statement, having produced those vegetables would make your financial position look worse. So you would make a $2,000 positive adjustment to your revenue to even that out.

On the other hand, if you end the year with no cleaned and packaged vegetables, you would have decreased your saleable inventory by $1,000, and you would make a $1,000 negative adjustment to your revenue.

Likewise, if you didn’t pre-sell any CSA shares last year for the current year, but this year you sold ten shares at $575 each in October for delivery next May, you’ve taken in an extra $5,750 in cash revenues – and that sure looks good on the bottom line for the current year! But while you’ve improved your cash position, your farm hasn’t actually performed $5,750 better this year than you did last year, so you would take a $5,750 decrease in revenues.

If you had two beds of garlic under a nice layer of mulch on January 1, but now, on December 31, you’ve got five beds of garlic, you’ve increased your crop production expenses, but haven’t had the opportunity yet to realize any revenues from those expenses. Now it looks like you’ve done worse financially this year than you did in the previous year, because you’ve spent more money growing garlic than you did last year; so you would adjust your expenses downwards by the amount of money you have into growing the additional three beds of garlic.

(In most of the agricultural world, stored crops are ready for sale; everything else is still “growing,” even if it’s corn standing in the field. Growing crops are valued at the cost of the inputs for those crops up to the current date; I recommend you value stored crops that aren’t ready for sale in the same way.)

You’ll also make adjustments to your revenues and expenses based on changes to accounts receivable and accounts payable, as well as your supply inventory. We’ll cover these changes in more detail next month.

When you make these adjustments to your net cash income, you get the net operating profit for the year.

Next, you should account for depreciation. Depreciation doesn’t take money out of your pockets each year, but it is real cost to your farm business. Don’t use the depreciation from your taxes – that doesn’t have anything to do with how much of your assets you’ve actually used up in the current year. Instead, calculate the actual depreciation using the formula ( purchase price – salvage value ) / life of investment = actual annual depreciation. The salvage value is how much you can sell the asset for at the end of its life on your farm. For the life of the investment, I recommend using a factor of 7 for equipment, and 20 for buildings.

Your net operating profit, less depreciation, equals your net farm income from operations.

Finally, account for changes to capital by adding up our capital purchases for the year – maybe you bought a used tractor for $8,000 and a new potato digger for $3,000, for total capital purchases of $11,000 – and subtracting any capital sales for the current year. If you bought a used tractor for $8,000 and a new potato digger for $3,000, and sold your old flail mower for $2,000, you would have total capital changes of ( $8,000 + $3,000 – $2,000 ) = $9,000.

Your net operating profit, less depreciation, plus the capital changes, equals your net farm income for the year.

The Statement of Cash Flows Where the balance sheet showed us all of the farm’s assets and liabilities, and the income statement helped us understand our annual cash revenues and expenses as well as operating profits, the statement of cash flows tells us what’s happening with that most necessary of commodities, our cash. It shows us all of the money that flows into the farm, whether it comes from selling vegetables or a loan from the bank. It shows us all of the money flowing off of the farm, whether it’s for servicing debt or paying for expenses. And by organizing those flows into discrete categories, it helps us understand where the cash is coming from, and where it’s going.

Where the balance sheet showed us all of the farm’s assets and liabilities, and the income statement helped us understand our annual cash revenues and expenses as well as operating profits, the statement of cash flows tells us what’s happening with that most necessary of commodities, our cash. It shows us all of the money that flows into the farm, whether it comes from selling vegetables or a loan from the bank. It shows us all of the money flowing off of the farm, whether it’s for servicing debt or paying for expenses. And by organizing those flows into discrete categories, it helps us understand where the cash is coming from, and where it’s going.

The statement of cash flows has three categories: cash flow from operations, cash flow from investing activities, and cash flow from financing activities. Each element has cash inflows and cash outflows.

In cash flow from operations, the inflow is the same as the cash revenues from the income statement. Because we’re only looking at what happened to our cash, rather than the financial performance of our farm, we don’t make the same adjustments that we did on the income statement.

The outflow is equal to the cash expenses from the income statement with the interest added back in. In the statement of cash flows, we don’t include interest in the cash flow from operations because it is a cost of financing, and therefore goes in cash flow from financing activities.

Cash flow from investing activities comes from the investments you make in capital assets. When you sold that $2,000 flail mower, that created a $2,000 inflow of cash; the purchase of the tractor created an $8,000 outflow of cash.

Cash flow from financing activities represents the cash that flows in to and out of your farm business from the entities that provide financing for the farm business – usually your banker, and the farm owner.

Loan proceeds – the money you borrow from the bank – provide an inflow of cash. Loan payments, including principal and interest, are cash outflows.

You may or may not choose to include off-farm income as part of your statement of cash flows. Most agricultural lenders will want to see your non-farm income included on a statement of cash flows, especially if your farm is a sole proprietorship.

The statement of cash flows should also show the money that you, as the farmer, are taking out of the business, either as family living expenses or as an owner’s draw. This owner’s draw would also include your payment of income taxes and social security taxes for your income.

The statement of cash flows shows you the net change in cash for your business. It is possible to run a business at a profit and still go broke if you don’t have the cash to service your debt, or if you make investments that you can’t afford.

Chris Blanchard helps farmers and food businesses create and improve systems to enhance profitability and quality of life. The host of the Farmer to Farmer Podcast and owner of Purple Pitchfork, he was worked in farming for the past 25 years, and has managed farms around the country. As the owner from Rock Spring Farm for fifteen years, Chris raised twenty acres of vegetables, herbs, and greenhouse crops, marketed through a 200-member year-round CSA, food stores, and farmers markets. His newsletter, The Flying Rutabaga, can be found at www.purplepitchfork.com.

Copyright Growing For Market Magazine.

All rights reserved. No portion of this article may be copied

in any manner for use other than by the subscriber without

permission from the publisher.