By Chris Blanchard

Knowing that you’ve got money at the end of the year means that you’ve done okay in the market farming game. But if you want to do better — if you want to put your effort into those crops that make the most difference to your bottom line — you need to know how much it costs to grow and market your crops.

If you sell at a farmers market or to stores and restaurants, you’ll want to know that you are making money on each crop, not just on your offerings as a whole. And you’ll want to know what crops to push, and where you should raise your prices or discontinue a product.

Even with crops grown for a CSA, understanding the results from each dollar and each hour spent can help you evaluate pricing your program, or provide a strong explanation for why your members have to pick their own peas. Knowing your costs can also help you evaluate the potential effects of growing your CSA. And if producing that pint of Sungold cherry tomatoes is costing a quarter of the value of your box, you may want to reconsider that crop’s role on your farm.

And it’s not just a matter of comparing crops within each marketing channel. Understanding how the costs required to sell at farmers market compare to the time put into writing newsletters and delivering CSA boxes will enable you to make smart decisions about pricing, expansion, and new directions when your circumstances change. When my partnership dissolved at Rock Spring Farm, I felt comfortable letting go of farmers markets in favor of CSA and wholesale because my analysis showed that farmers market sales provided a much lower margin when expenses, including unpaid labor, were added.

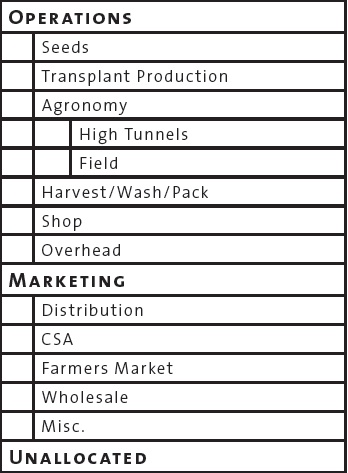

Production and Marketing

For every crop grown on a market farm, crops follow a more-or-less set pattern as you change seed, soil, and sunshine into cash. By defining the steps in the pattern, you can define the basic unit of each step — acres, dollars, transplants, pounds — then develop a cost per unit. Adding up the costs gives you a basic cost of production.

The steps in the pattern of producing a crop include seeds, transplant production, agronomic work in the field and high tunnel, and harvesting, washing, and packing the produce. For production, each step in the process has a substantially similar cost structure. For example, seed costs are made up of seeds and shipping; and the inputs for producing a tomato transplant are the same as those for producing a broccoli transplant. By dividing the production process into a series of steps, you can isolate those expenses that are the same for every crop, and notice the expenses that are substantially different for specific crops.

The process of turning a finished product into cash also follows a reliable pattern of marketing, sales, and distribution. Each marketing channel your crops follow will have different costs associated with it: a weekly newsletter for the CSA, packaging requirements for wholesale sales, or the costs of driving to farmers market and renting a stall.

Data to pull together

You’ll need four kinds of data to derive your cost of production: the crop-specific expenses for each step in the production and marketing process; the universal expenses for each step; the number of units you used in each step in the process; and how much of each crop did you sell?

Seed costs vary widely by crop, and can be one of the most frustrating data points because it usually consists of a large number of small purchases. If you can track these as you go, using a spreadsheet or a simple database, you’ll be miles ahead in December. For the most accurate information, you should track the amount of seed you use over the course of the season for each crop, and do some math to figure out the cost of the amount of seed you used, plus any you discarded.

Allocate Transplant costs to get a number for how much it costs to grow each transplant. You’ll want to know the total number of transplants you grew of each crop. Costs include items such as potting soil, heating costs, and labor to water and move transplants. I include the labor to set out transplants as part of the cost of transplant production, since it takes significantly more time to put out transplants than it does to direct seed a crop.

If you plant multiple seeds per cell for some crops, that’s still just one transplant in terms of the costs of production. If you seed something like onions in a straight flat, use the cell count of the equivalent-sized cell tray to get the number of units used.

Some crop-specific costs in transplant production could include activities such as grafting tomatoes, stepping plants up to very large pots, using expensive peat pots, or the extra labor associated with sticking perennial cuttings.

Agronomy includes all of the cost to work the fields, build fertility, weed, and do everything up to the point somebody puts a hand on a vegetable to pick it. You’ll get pretty close if you allocate the cost of operating your machinery and doing most of your hand-weeding across all of your cash crop acres; unless you’ve got really amazing records, it’s going to be hard to drill down to by-crop differences. Your end results should be expressed in a cost per acre.

I don’t try to allocate the cost of something like growing a preceding cover crop to a specific cash crop, but I do allocate the costs of crop-specific inputs, such as mulch or trellising supplies.

You will also need production records that tell you how many acres you planted to each crop. Because you are getting at the cost of production, you don’t need to know how many acres you had in headlands or cover crops; the costs of growing and maintaining those areas will be allocated to the acres where you actually produced a cash crop.

Harvest, Wash, and Pack captures all of the expenses from the time somebody puts a hand on a vegetable to pick it right up to the point expenses or labor start to differentiate by marketing channel. Several years ago, we undertook a bagged carrot enterprise. We allocated the costs and labor for harvesting and washing carrots to Harvest, Wash, and Pack; we also allocated the labor to put them into boxes or bins. We allocated the cost of the boxes and the labor to bag the carrots as crop-specific “marketing” costs for the different marketing channels.

Because Harvest, Wash, and Pack costs vary dramatically by crop, you’ll want to sample some harvest and packing times throughout the season. Combine the results of your sampling with your sales information to get total cost for each crop’s harvest, wash, and pack inputs.

We track cost allocations for activities in the farm’s Shop, and allocate those by acre to each crop. Overhead expenses — such as the expense to operate the farm car, or computers in the office — are allocated according to the percentage of income provided by each crop.

Tracking expenses associated with each marketing channel can provide valuable insights. The expenses for a particular marketing channel begin when you start to do something different, as in the carrot bagging example above.

You’ll need your sales records for each marketing channel so that you know how much of each crop you sold. You’ll also need records for the expenses associated with each marketing channel, such as the boxes required to sell wholesale, the cost of a website for potential CSA members, or the labor to drive to and staff a farmers market stall.

When it comes to Distribution, allocating expenses between different marketing channels can present real challenges. One farm I worked for in my early years took CSA, wholesale, and farmers market crops to market in one trip with a large refrigerated truck. In this case, allocate distribution costs among different marketing channels according to how much space they occupy on the truck; estimating by pallet will be close enough.

At Rock Spring Farm, we spent years combining CSA and wholesale loads on one delivery run. Even though some stops were strictly wholesale, some were strictly CSA, and some were mixed, we only split our allocation according to the load, rather than trying to figure out which miles belonged to the CSA and which belonged to wholesale.

Ownership Costs

For many of the links in these chains, you’ll need to allocate the costs of owning equipment or facilities. If you bought a rototiller last year, that investment should last you a very long time. You can’t expect it to pay for itself in just one year. To allocate ownership costs, use the following formula, in which the salvage value is the price you could get for the equipment after the useful life of the investment:

As much as possible, you should also allocate the costs associated with owning an asset to the step in the production and marketing process where the asset is used. For example, allocate the insurance costs for your tractors to agronomy, and the costs of insuring the packing house to the harvest, washing, and packing step.

Valuing Labor

Most farms have two kinds of labor: the farmer’s, and everybody else’s. Hired labor should be valued at the actual cost of an hour of labor: along with the basic cost of wages, you want to include taxes, worker’s compensation insurance, payroll processing recruiting expenses, health insurance, and donuts.

You also have to account for your own labor to arrive at a meaningful cost of production and marketing. I suggest including your labor at the cost you pay your crew. Returns above that base wage represent the profits you earn for your entrepreneurial ability, tying up your cash in farm assets, and taking the risks associated with owning a business.

QuickBooks Data

To track much of this information throughout the year, I use the Class feature in QuickBooks. Turning on the class feature allows you to organize transactions in two ways – Account and Class – instead of just one. All income gets allocated to one of the Marketing classes in the list below; all expenses are classified in either Operations or Marketing.

When I don’t know how an expense like a fertilizer purchase will be allocated between high tunnels and field production, I use the next level up in the hierarchy; in this case, I would assign the fertilizer purchase to Agronomy, and use my production records to determine the correct allocation at the end of the year.

Cost of Production

You can use the information gathered above to establish a total cost for each step of the production process. The total cost minus the crop-specific expenses gives you the non-crop-specific costs for the step; that divided by the units gives you the cost per unit. For example:

To determine the total cost of the Agronomy step for tomatoes, you would multiply the base cost per acre by the acres of tomatoes you grew, then add any expenses that were specific to growing tomatoes, such as the ownership cost of tomato stakes, the cost of the twine for trellising, and the cost of the labor to do the trellising work.

Marketing Costs

Once you’ve established the cost of production for a given crop, you can use the same math to establish your marketing costs in each marketing channel.

You might find it useful to think about marketing and distribution as a separate division of your agribusiness enterprise: in this model, each marketing segment “buys” the crop at the cost of production, then sells it for a margin above that cost. That margin has to cover all of the expenses associated with selling that product through that particular channel, as well as providing a profitable return. You can calculate the gross margin using this formula:

In addition to establishing the gross margin for each crop sold through a particular channel, you can use this same formula to establish your gross margin for the entire marketing channel, enabling you to make informed choices about shifting your marketing strategy.

You’ll also want to establish a break-even price for your product in each marketing channel you sell through. You can calculate a break-even price using this formula:

Valuing crops in a CSA, and therefore establishing a gross margin and a break-even price, presents some special challenges since crops aren’t sold as individual items, but instead as a package of products. But if you market crops through other channels in addition to your CSA, you’ll want to understand your gross margins in the CSA relative to other channels.

You can choose any number of methods for establishing a base “price” for a CSA crop: you can use farmers market prices, grocery store prices, or a wholesale price list. Use these prices with your packing records to establish a total base value for your CSA sales; your CSA share price divided by that base value, multiplied by the base price of a given crop, will give you an adjusted sales value for each crop.

By estimating your costs and returns for crop production and marketing channels, you’ve positioned yourself to make decisions about crop mix, marketing outlets, and pricing from an informed perspective.

Chris Blanchard owns and operates Rock Spring Farm in Northeast Iowa, and offers education and consulting as Flying Rutabaga Works (www.flyingrutabagaworks.com). He is the co-author of Fearless Farm Finances: Farm Financial Management Demystified, available from http://www.mosesorganic.org/farmfinances.html.

Copyright Growing For Market Magazine.

All rights reserved. No portion of this article may be copied

in any manner for use other than by the subscriber without

permission from the publisher.